-1783304403050.jpg)

The case for micro enterprises: Driving national and economic growth

By Visa

Research insights from Visa Government Solutions highlight the transformative potential of digital payments in driving economic empowerment and inclusion for micro and small enterprises (MSEs), a vital subset of the broader micro, small and medium enterprises (MSMEs) sector.

Digital payments provide viable pathways for the sizable MSMEs sector to be more integrated in local economies. Image: Canva

Across ASEAN Member States, MSMEs (micro, small and medium enterprises) account for between 97.2 to 99.9 per cent of total business establishments. Collectively, MSEs (micro and small enterprises) and MSMEs contribute 85 per cent to employment, 44.8 per cent to GDP and 18 per cent to national exports, underscoring their central role in regional economic and social development.

While MSEs operate on a smaller scale, their economic and social impact is equally significant. Yet there remains a notable gap in available data. Globally, emerging markets host an estimated 55 to 70 million formal microenterprises and 285 to 345 million informal enterprises. This lack of visibility poses challenges for policymakers seeking to unlock the full potential of MSEs.

To bridge this gap, governments and stakeholders should take deliberate steps to include and empower MSEs in economic planning. A recent research paper by Visa, in collaboration with ODI Global Advisory, explores how digital payments can be a catalyst for MSE growth and integration into the formal economy.

Empowering MSEs through digital payments

Digital payments can provide MSEs with a gateway into the formal financial system. The adoption of digital payment solutions can help these businesses to strengthen their access to credit and financial services, unlock opportunities to raise productivity, increase income and invest in growth.

In Colombia, for example, mobile wallet transaction histories are now being used to assess creditworthiness, enabling microentrepreneurs to secure formal loans that were previously out of reach.

However, the transition is not without challenges. Some MSEs are reluctant to adopt digital payments due to concerns about increased tax obligations, higher operational costs, administrative burden of compliance and reliance on intermediaries.

In many markets, mistrust of formal institutions is deeply rooted. This is shaped by long-standing socioeconomic inequalities and perceptions that banks and government programmes do not prioritise the needs of microentrepreneurs.

In South Africa and Colombia, for instance, some MSE owners view government-led digital payment initiatives as being driven more by taxation goals than by genuine business support.

Despite these concerns, global examples demonstrate the transformative potential of digital payments.

In Panama, national growth strategies include expanding access to information and communication technology (ICT) to boost MSE productivity.

In Ethiopia, the focus has been on enhancing the capabilities of tourism SMEs, improving the tourist experience through digital innovations.

Across these cases, a common theme emerges in which digitalisation drives productivity and competitiveness.

To subscribe to the GovInsider bulletin, click here.

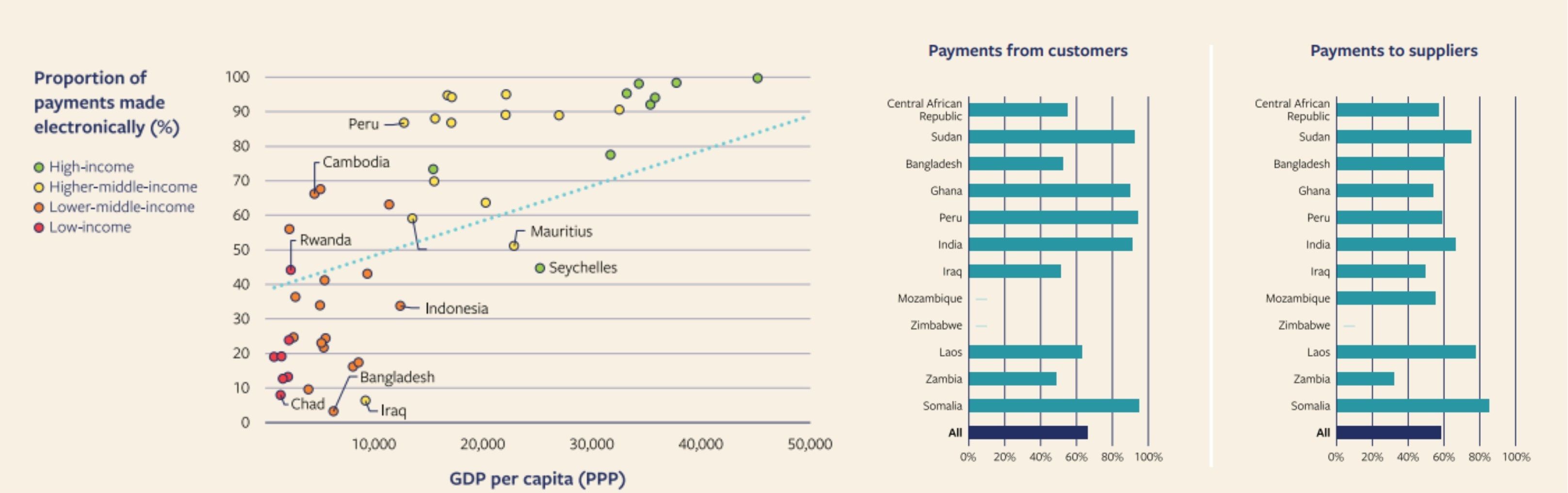

Use of digital payments by MSEs

Recent data from the World Bank Enterprise Surveys reveals a strong correlation between a country’s income level and the adoption of digital payments.

Higher-income economies tend to see greater usage among small enterprises in the formal sector, though there are exceptions. Cambodia, for instance, outperforms the average for its income group, while Indonesia falls below it.

Interestingly, even in lower-income urban economies, more than 60 per cent of informal enterprises report using mobile money for customers and supplier transactions. This suggests that many informal enterprises have already recognised digital payments as essential to day-to-day operations.

A pathway to formalisation and inclusion

Overall, these findings support the view that digital payments are a vital pathway for MSEs to enter the formal financial system. While many informal enterprises are already on this journey, policymakers play a critical role in accelerating the transition.

At the same time, authorities need to balance economic growth objectives with an understanding of social realities, ensuring that initiatives are inclusive, build trust and address the needs of the communities.

This is the first of two articles on Visa Government Solutions’ micro and small enterprises research insights. You can read the full research paper here.